-

The Fine Line! (Our government is hunting down someone who simply exposed how they “government” were illegally spying on all of us.)

Have you ever wondered what makes a person snap? What causes a normal, quiet, everyday citizen, loving mother, or doting father to lose it all and fight like a caged animal? What can cause a small village to rise up and rebel against an oppressive police force and start killing them? What is the switch that gets flipped that causes a city to pour two million people into the streets, chanting and demanding to be heard by their government?

Lately it feels more and more as though we are on standing on the edge of some yawning precipice peering over the crest into darkness. What is more troubling to me is that we have been down this path before. The sense of unease is almost palpable to me sometimes; it is more evident if you are paying attention. If you are able to eliminate the white noise of the world for a minute; hit the pause button on the playlist of daily life for a while and look around, listen, you may start to recognize that you too are caught up in events that will soon change all our lives.

For several years I have felt an unsettling sense that we need to be prepared, that life is going to throw us a big, fat, greasy curve ball soon and we better not be caught napping. To try and proactively address that warning voice I started planning and taking steps to prepare my family to be able to weather events in the future. I am certainly not alone in this concern as you can easily see by the tremendous growth of the prepper movement. In the spectrum of probable events, there are a lot of potential scenarios. Natural disasters and emergencies occur every day all over the world, but you have to broaden your gaze and look to current events and history as well. One of the things that I think is a valid potential event to consider is a collapse of our way of life which leads to an authoritarian oppressive government.

Are we reaching a tipping point?

SS soldiers guarding the column of captive Jews in the Warsaw ghetto. We have seen in recent events, by now almost too numerous to mention, the effects of a rising frustration with the way things are. It isn’t necessary to go into all of the individual reasons, but as a society there are more and more outpourings of frustration on a global scale. There are increasingly tightening restrictions against people. There is a manipulation of markets and the economy. There is a great increase in the loss of freedom and there is a more open antagonism and almost outright animosity by Government towards their people.

Governments exist either because they have come to power through force and violence or they have been elected and given power by the people. The force and violence crowd usually have their roots in the military and we like to call them Dictators. There have been a ton of them throughout history; Hitler, Stalin, Mao, Kim Jong iL and now his son, Saddam, Gaddafi, the list goes on and on. Dictators don’t care about the people and usually kill anyone who gets in their way. It is a fact that government has killed more people than any other cause, disease or reason.

The other side of the coin is what is usually called Democracies. I am lumping a lot of governments in here I know, but the democracies are usually elected and formed with the consent of the people with the noble goal of securing rights or protecting the people over whom they govern. Almost without fail however, Democratic Governments eventually do not want to answer to the people and at some point they most certainly will not be told what to do by the people to the point of ignoring the will of the people (for the people’s own good of course). Now these governments that are supposed to secure the liberties of their people are becoming more openly hostile to the same people they have sworn to defend. Funnily enough the democratically elected governments now seem to want to hang on to power with the same methods of force and violence as dictators. How else can you explain arming themselves with ammo, ignoring the constitution, purchasing assault vehicles and preparing to confiscate firearms?

When governments will steal money outright from the citizens in order to pay bills that were not incurred by the people we have a problem. When government spies on its people and uses that information against them punitively we have a problem. When Government uses the force of the military that was supposed to defend the people that was paid for by the people, for the purposes of killing the people, we have a big problem. When someone brings to light crimes by the government and is labeled as the one who is a danger, we have a problem.

The problem is that governments around the world are viewing their people as the problem and there really seems to be only one way throughout history that this is ever rectified. My fear is that we are already set on a course that won’t be changed with laws, great political leaders, or a return to the values of a golden age in time long past.

The Fine Line – The Straw that breaks the camel’s back

The fine line between someone who is a law-abiding citizen and a murderer is one that exists purely in our souls. There is nothing physical that is different from a person who follows the rules and someone who breaks them. The urge to pull the trigger isn’t something you can see and it isn’t a trait to test for, so it must be our own individual sense of right and wrong. Of good and evil.

I know that some will argue that a psychopath is definitely recognizable by character traits and maybe even brainwaves or chemistry. That may be true, but you can be a psychopath (clinically) without ever hurting anyone. By the same token, you can take a life while being perfectly “sane”.

If you hold a knife in your hand, you are just as capable of using that to stab or cut someone as the murderer in the next town, but that thought never enters the mind of an overwhelming majority of people. A baseball bat in your hands can easily be swung with great force connecting it to the back of a skull, but this thought never appears in our heads; that is unless we are forced into a corner. When a person is in desperate fear for their lives, the unspoken rules of right and wrong are broken. The processes that we follow every day are overridden in the cause of rage or self-preservation. What was unthinkable before is now very real, necessary and even righteous with the right circumstances.

When the right buttons are pushed, anyone can lose it. When the fear of dying or of losing someone you love is so overpowering, the “fine line” that has been keeping us sane, law-abiding and good is easily shattered. When this happens, all bets are off.

We as a people, a country are still rather firmly attached on the good side of this line. We have not yet completely been driven to abandon all hope and lash out. We have not yet been so harmed, have not gotten to the point that we have nothing to lose and are ready to lose it, but this may be coming in the future.

The force and violence that is being used now to quell the dissatisfaction of people globally is increasing. The methods to cease the complaining of the rabble has been relatively minor with some exceptions. Tear gas, rubber bullets, mace and batons only work up to a point though. When the time comes that people can no longer abide, there won’t be enough police to stop them using riot control techniques. The military doesn’t have enough people to stop the entire population unless those people peacefully agree to surrender, so what will they do? Do you believe any government will quietly step down and admit that they are obviously not speaking for the people anymore? No. They will resort to more force and violence and people will die. Either that or you have a coup like they had in Egypt and guess who took over to “restore order”? Yep, the Military.

What will be the inevitable response by the authorities?

The Chinese people who started to revolt against the police in their town did so because the authorities were “placing restrictions on their culture, language and religion”. China is no picnic compared to America and we clearly know they have lived through far worse oppression than we have, but this was the straw that broke the camel’s back for them?

The protests which turned into an estimated two million citizens of Brazil had started simply enough with a protest over a rise in the rates of public transportation.

In America, what will be the trigger that causes people to rise up and say we aren’t going to take this anymore and more importantly what will happen when/if we do?

What will happen if we don’t change the path we are on?

The execution of the last Jew in Vinnytsia, made by an officer of the German Einsatzgruppen There is a quote that has always struck me as very sad and telling from Aleksandr Solzhenitsyn in his book The Gulag Archipelago. Solzhenitsyn was a Russian who was sentenced to 8 years in a Soviet prison camp for essentially writing things about Stalin that the government didn’t like. During this time in Soviet Russia, to stifle dissent, millions were killed or sent to prison camps. In this passage Solzhenitsyn is talking about regret that everyone felt because they simply went along with this tyranny and didn’t oppose it.

“AND HOW WE BURNED IN THE CAMPS LATER, THINKING: WHAT WOULD THINGS HAVE BEEN LIKE IF EVERY SECURITY OPERATIVE, WHEN HE WENT OUT AT NIGHT TO MAKE AN ARREST, HAD BEEN UNCERTAIN WHETHER HE WOULD RETURN ALIVE AND HAD TO SAY GOOD-BYE TO HIS FAMILY? OR IF, DURING PERIODS OF MASS ARRESTS, AS FOR EXAMPLE IN LENINGRAD, WHEN THEY ARRESTED A QUARTER OF THE ENTIRE CITY, PEOPLE HAD NOT SIMPLY SAT THERE IN THEIR LAIRS, PALING WITH TERROR AT EVERY BANG OF THE DOWNSTAIRS DOOR AND AT EVERY STEP ON THE STAIRCASE, BUT HAD UNDERSTOOD THEY HAD NOTHING LEFT TO LOSE AND HAD BOLDLY SET UP IN THE DOWNSTAIRS HALL AN AMBUSH OF HALF A DOZEN PEOPLE WITH AXES, HAMMERS, POKERS, OR WHATEVER ELSE WAS AT HAND?… THE ORGANS WOULD VERY QUICKLY HAVE SUFFERED A SHORTAGE OF OFFICERS AND TRANSPORT AND, NOTWITHSTANDING ALL OF STALIN’S THIRST, THE CURSED MACHINE WOULD HAVE GROUND TO A HALT! IF…IF…WE DIDN’T LOVE FREEDOM ENOUGH. AND EVEN MORE – WE HAD NO AWARENESS OF THE REAL SITUATION…. WE PURELY AND SIMPLY DESERVED EVERYTHING THAT HAPPENED AFTERWARD.” – ALEKSANDR SOLZHENITSYN

Will this be our fate too? Will we slowly be conditioned to accept atrocities like this and to be completely defanged so that we can be herded into camps without so much as a whimper as well? That’s crazy you say! Is it? Right now, our government is hunting down someone who simply exposed how they (government) were illegally spying on all of us. Our government is buying arms and stockpiling weapons for use domestically not in some war. Our government has the IRS actively harassing a single political/opposition party. Our government has shown that they will lock down a town and go door to door while making the citizens stay cowered inside. Our government has stated that they can imprison anyone without cause for an indefinite amount of time.

Can you seriously argue that we aren’t headed down the same path as others have in our not too distant past?

This is not a call to armed Revolution, but I do think we should all be very wary of this course we are on and the echos of history. We should not be silent in the face of increasing oppression. We should not simply go along quietly because of the fear that we may get in trouble, or worse that we believe the government is only looking out for our best interests. You only need to look at the people in Poland who quietly went into the Warsaw ghettos. You don’t have to look any further than the Holocaust to see what quietly going along will get you.

This is not a fate that I will be bringing on my family.

You can also access the latest news at this address: www.whatfinger.com

-

Why Did 10 Million Americans Lose Their Homes After The 2008 Financial Crisis?

According to: investopedia.com- In many ways, the American Dream is a concept of optimism. It implies equal opportunity and that any individual can aspire to financial stability and even superior wealth—regardless of their background—through hard work, entrepreneurial ventures, or other means. A large component of financial stability and the American Dream is owning your own home. The Great Recession and the ensuing housing collapse in 2008 cast doubt on the so-called “American Dream.” The economic crisis precipitated by the 2020 lockdowns and job losses didn’t help.

When we solve a problem, after a while, we tend to forget what solved the problem and go back to what we used to do that caused the thing to go over the cliff in the first place.

That was the 2008 mortgage and financial crisis, as it forgot the lessons of the Great Depression.

History up to the Great Depression

In the 1920’s, when the economy was booming and it seemed like the party would never stop, banks lent out a ton of money on credit, with the presumption that all that money would be paid back and that there was sufficient collateral to cover it.

Except, there wasn’t.

One of the biggest assets that people might own that a bank could recover is real property. As Will Rogers once noted: “Buy land. They ain’t makin’ any more of the stuff.” Real property was something that pretty much always appreciated in value.

Prior to the early 1900’s, most people didn’t own their own homes. Most people rented. Many lived in tenements and apartments in cities, or lived as tenants on farms in rural areas. Land speculators often bought what was left of the government land grants as the frontier closed.

But, in the 1920’s, that began to change as banks felt more confident in lending credit for new construction. There were significant speculation bubbles. People bought property and built homes on future credit that wasn’t based on anything but hope.

And as the stock market ticked ever higher and higher, banks bet on it. With the deposit money of their customers.

And then the Stock Market Crash of 1929 hit.

Banks that were significantly overleveraged and undercapitalized were hit hard. Many just failed, and those who had their deposits at banks that became insolvent just lost everything. There was no deposit insurance. If your bank went under, you were screwed out of your entire savings.

And if you lost your job, that meant you also lost any means of continuing to pay back that home loan.

Additionally, there were suddenly vast quantities of new construction for sale… that nobody could afford any longer. That drove down property values everywhere.

Suddenly, your property that was worth $10,000 last year might now only be worth $5,000. But you might still owe $8,000 – what we call “underwater.” If you default or declare bankruptcy, the bank loses. And you’re out on the street.

And then, what could the bank do with the house? How could they sell it? Nobody was buying. So, the bank suddenly has a ton of illiquid assets.

More foreclosures in a neighborhood continues to lower the property values further, and the destructive cycle just ends up repeating itself.

The Hoover administration tried economic protectionism. At the administration’s pushing, Congress passed the Smoot-Hawley Act of 1930, which imposed schedules of high tariffs on over twenty thousand types of imported goods, to protect American business, by golly.

It backfired spectacularly and greatly exacerbated the worsening Depression.

Weather conditions didn’t help. A severe drought ravaged the Midwest and Great Plains starting in 1930. Farmers had been using what in retrospect were poor farming practices, tearing down line fences and forest windbreaks and not planting cover crops for winters. The thin layer of good topsoil in the Great Plains turned to dust and became an ecological nightmare.

Farms started going under as crops failed. The Smoot-Hawley tariffs only made things worse.

Additionally, the money supply dried up. The banks that survived, like J.P. Morgan Chase, just turned off the credit spigot to stay afloat. They stopped lending. Why? Again: illiquid assets. The banks were holding on to all these properties and other assets that they couldn’t sell. And people didn’t trust the banks because so many had lost everything depositing their savings there. Because the banks couldn’t sell anything they had, and nobody would give them any cash, they didn’t have any money to give out.

Part of the problem was the gold standard. Under the Federal Reserve Act, at least 40% of the money in circulation had to be backed by gold reserves held by the federal government. So, there was no modern tool of being able to print more money to help increase liquidity.

On top of that, gold became more expensive. Mortgages often had clauses that allowed banks to demand repayment in gold because of the gold standard. By 1932, that resulted in a disparity in payment between the dollar and the value of gold that meant that if a debtor was forced to repay in gold, it could cost him as much as $1.69 for every dollar he owed. This led to more bankruptcies and foreclosures still.

Because of the tariffs, the lack of money supply, the collapse of agriculture, and lack of consumer spending, rampant deflation initially set in. This made exported American goods increasingly more expensive for overseas importers, even where other nations had not instituted retaliatory tariffs of their own. Manufacturing began to collapse. The steel industry followed.

And the Depression spiraled out of control.

When Roosevelt took over from Hoover in 1932, the nation was becoming increasingly desperate.

The New Deal

Roosevelt ran on a radical new idea that he called “The New Deal.” The premise was that the government would intervene in the economy and prop it up through deficit spending and government borrowing. The New Deal would create government programs to put people back to work and get people back to farming and building things, and that eventually, once people got back on their feet, the government could take those supports out.

Various New Deal reforms were leveled at the financial sector to try to get the credit flowing again.

One reform was put on the banks directly: the Glass-Steagall Act. One of the problems with the banking crisis was that banks could gamble with depositor’s money. The Glass-Steagall Act separated investment banks from commercial banks. Investment banks are gamblers. These deal with stock and bonds and venture capital and hedge funds and Wall Street. Commercial banks are the Savings and Loan where you put your nest egg. The Glass Steagall Act put a firewall between the two. The idea was that Wall Street could melt to the ground and Main Street wouldn’t go with it.

Keep this in mind. It will be important later.

Another was to protect depositors. Commercial banks would be required to pay into a new Federal Deposit Insurance Corporation: the FDIC, which would make sure that depositors would get paid back if the bank collapsed. That encouraged people to trust banks again. People would deposit their money, and banks could use that money to start giving out loans again.

A third was to help reduce the risk of default on certain types of loans through surety agreements. Sureties had been around forever: they’re a promise to pay a debt if the original debtor defaults.

The Federal government aimed these programs at home loans in particular, to try to reduce the homelessness problem. And so, in 1938 with the National Housing Act, the government formed the Federal National Mortgage Association, or FNMA. FNMA, or “Fannie Mae,” would buy the mortgages from the banks, who would continue to “service” the mortgages. From the perspective of the consumer, it looked just like their ordinary transaction: get a loan from the bank, pay the bank. The bank kept some money for “service fees,” and the Feds took over the loan, and importantly: the risk of default. This created a secondary market for mortgages for the first time in history.

But Fannie would only buy that mortgage if it met certain criteria, such as debt to income ratios, term of the loan, and more. If banks wanted to make other loans, that was fine, but Fannie wouldn’t buy them.

And the program basically worked. Banks started lending again. Credit slowly started to thaw out. Banks started getting more liquidity in their balance sheets. People started being able to buy homes again.

After World War II, the housing market took off again, fueled in part by the GI Bill and a push for suburbanization and the creation of easily duplicated, cheap ranch houses on a standardized template.

But in the background still driving things along was always Fannie Mae and the prime 30 year fixed-rate mortgage, which had become as much a part of the standardized American experience as baseball. Housing prices rose steadily home ownership became a stable part of the American economy. Virtually every person in the country could see a viable path to owning their own home.

By the 1960’s, FNMA owned more than 90% of the residential mortgages in the United States and individual home ownership had risen to the highest levels ever recorded. This led to the greatest expansion of the middle class in history.

So, of course, like all wildly successful government programs, we had to fix it.

Privatization

In 1954, FNMA was semi-privatized into a public-private hybrid where the government owned the preferred stock (with better voting rights within the corporation,) and the public held the common stock (which gave dividends, but inferior voting rights).

And in 1968, Fannie Mae was privatized entirely, with a small slice of it (known as Ginnie Mae) carved off to maintain Federal Housing Authority loans, Veterans Administration loans, and Farmer’s Home Administration mortgage insurance. Because Fannie Mae had a near monopoly on the secondary mortgage market, the government created the Federal Home Loan Mortgage Corporation to compete with it: Freddie Mac.

By 1981, Fannie and Freddie were doing well as private companies, and Fannie came up with a great idea that had been done in limited settings: pass-through mortgage derivatives. They would bundle up various mortgages and sell them as a type of bond to investors. Investors loved the idea. The housing market had been extremely stable for nearly fifty years and offered a modest, but highly reliable return. And so the commercial home loan mortgage backed security was born.

Keep this in mind. It will be important later.

The Savings and Loan Crisis

By the early 1980’s, the economy had been stable for 30 years (more or less,) and thanks to the Glass-Steagall Act, commercial banks were doing okay even with the “stagflation” of the 1970’s. Home prices continued to rise about on par with wage growth.

But one type of commercial banks, the Savings and Loan banks, wanted to do better than okay. S&L’s were the kind of bank in It’s a Wonderful Life. S&L’s were specifically singled out in federal legislation, like credit unions, for a single purpose: to promote and facilitate home ownership, small businesses, car loans, that sort of stuff.

A business-friendly Congress agreed. They passed two laws in 1980 (signed by Jimmy Carter) and 1982 (Signed by Ronald Reagan) that allowed banks to offer a variety of new savings and lending options, including the Adjustable Rate Mortgage, and dramatically reduced the oversight of these banks.

Adjustable rate mortgages work by locking in a fixed rate for a short term, and then after that initial term, the mortgage rate would re-adjust every additional term after that. If the prime interest rates set by the Federal Reserve stayed high, lenders would get hammered.

But S&L’s had a fix in mind for consumers: just keep refinancing your home every time the first term is up. Home prices would just always continue to rise, right? They could collect closing costs every couple of years, and consumers remained essentially chained to them in debt with a steady stream of revenue that would always be secured if something happened. It was perfect.

Keep these types of mortgages in mind. It will be important later.

By the mid-1980’s, the lack of oversight allowed S&L’s to start making riskier and riskier decisions, offering certificates of deposit with wild interest rates, as much as eight to ten percent. They were exempted from FDIC oversight, while still keeping deposits federally insured (what could go wrong there, right?)

And then the Federal Reserve, in an effort to reduce inflation, raised short-term interest rates, which sent ripple effects through these S&L’s, who had been made very vulnerable to that particular issue through these bad decisions, lack of appropriate capitalization, and overpromising depositors.

By 1992, almost a third of savings and loan banks nationwide had collapsed.

This crisis led to the Financial Institutions Reform, Recovery and Enforcement Act of 1989 (FIRREA), which put back some of the same oversights that had been taken off because people wanted to make more money, particularly better capitalization rules (which were tied to risk,) increased deposit insurance premiums and brought back some FDIC oversight, and reduced these banks’ portfolio caps in non-residential mortgages.

Keep this in mind. It will be important later.

The Repeal of Glass-Steagall

Remember how back in the 30’s, in the midst of the Great Depression, we instituted that firewall between investment banks and commercial banks?

Again, it worked so well, we had to fix it.

Starting in the 1960’s, the federal regulators began to start to allow commercial banks to get back into the securities game again. The list was limited, and was supposed to stay in relatively safe stuff.

This accelerated under Reagan’s policy of deregulation, and continued under Clinton in the 1990’s. By 1999, Bill Clinton declared that Glass-Steagall no longer served any meaningful purpose, and most people had declared it dead well before that. The law was officially repealed in 1999 with the Gramm-Leach-Bliley Act.

Immediately, investment and commercial banks start merging again. Bear Stearns, Lehman Brothers, Citibank, all of these investment banks start buying out the commercial banks or merging.

And there’s a culture difference between those.

Remember: investment banks are gamblers. These are the Wall Street guys. They’re risk takers. They’re hedge fund managers. These are your Gordon Gekko type guys. Commercial banks are Main Street guys. They’re generally conservative, George Bailey types.

And the investment banker culture won out over the course of the 2000’s. George Bailey starts snorting coke and putting on Ray Bans with a blazer and jeans.

Sub-Prime, NINJA, and ARM Loans

In the early 1990’s, affordable housing started to become a greater and greater issue. George H.W. Bush signed legislation in late 1992 amending Fannie and Freddie’s charters to push them to make loans to people with lesser means than the traditional prime criteria. The Clinton Administration continued pushing Fannie and Freddie to accept more low and moderate income earners.

That meant taking on riskier loans.

The Clinton administration put rules in place in 2000 to curb predatory lending practices, and rules that disallowed those risky loans from counting towards their low-income targets.

The Bush administration took those predatory lending rules off in 2004, and allowed those risky, “sub-prime” mortgages to count towards the low-income targets set by Housing and Urban Development.

Remember those ARM mortgages?

Heh, heh. This is getting long, and you probably glossed over that, didn’t you? I told you it was going to be important.

Banks started making riskier and riskier loans, often those ARM loans. They could meet their HUD targets and make tons of money. And again: the gravy train was endless, right? The housing market had not lost value for over fifty years, even in the recessions of the 70’s and 80’s.

So, they put more people in houses. Bigger houses. More expensive houses. The economy was doing good. New construction was hot. Contractors couldn’t build the McMansions fast enough.

Banks started a race to the bottom with these sub-prime loans, getting all the way to NINJA loans: No Income, No Job, No Assets required. You’re a homeless person selling Etsy products out of your car? You’re already prequalified on a quarter-million subdivision home with a quarter-acre. Congratulations.

As long as you could afford the payments, you were in.

De-regulation

In the early 2000’s, the Bush administration wanted to keep the economy going. There was a low-level recession from March 2001 to November 2001 following the dot-com crash. The administration lifted a number of securities and financial sector oversight rules. One of those rules was about capitalization.

Remember that? I told you that was going to be important.

Capitalization requirements are how much reserve cash a bank needs to keep on hand to prevent collapse if something happens, against their liability sheets. Remember: that’s how banks got in trouble before the Great Depression and again right before the Savings and Loan Crisis. They took on too many liabilities and didn’t have enough capital to actually pay it all out.

The Bush administration relaxed the rules on required capitalization and what assets could count as capital. Some of those assets turned out not to be very useful.

Collateralized Debt Obligations and the Mortgage Backed Security

Remember, back in 1981, when Fannie starts issuing those mortgage backed securities, re-selling them as bonds with a low, but reliable interest rate?

That gets more complicated after 2004–2005 with the increased use of a financial tool called the collateralized debt obligation. Basically, a CDO is just a promise to pay investors in a sequence based on the cash flow from something the CDO invests in. The rate of return was tied to how risky the CDO was.

In the 70’s and 80’s, CDOs were pretty safe, mundane things. They were basically like index funds; they invested in a lot of stuff and did okay. But by the mid-2000’s, CDOs were becoming riskier and riskier, while providing more and more reward. CDOs bought up mortgages like crazy, because they had increasingly higher interest rates as the subprime mortgages started taking off.

But people were nervous about investing solely in these high-risk CDOs. And so, investment banks that bought up those mortgage-backed securities started to bundle together some high-risk mortgages with some regular, low-risk mortgages and promising that they were safer.

And then some investment banks started to lie about how many of those high-risk mortgages were in them. Why? Again: the housing market was super-stable and always going up. Those loans only looked high-risk on paper, right? I mean, those debtors could always just keep refinancing every couple of years.

So banks bought up those assets and added them to their capitalization sheets.

You see it, right? You see the problem here? Not yet?

Keep this in mind. It will be important in just a minute.

The Collapse

I remember being in college in the early 2000’s, and asking the loan officer at our local bank how some of the people I knew were making maybe $10–12 an hour could afford these massive homes and boats and jet skis and campers. My parents were teachers; they weren’t doing bad, but we couldn’t afford all that and I knew they were doing better than some of those people. The loan officer shook his head and said, “They can’t. They can afford the payments.”

Some of those people didn’t have furniture in their homes. If they had a party, they rented furniture for a couple days. I’m serious. That was a thing. Many of them were in deep, crippling credit card debt, paying off the balances of one with another, and justifying it with the idea that it would be okay when the next raise kicked in.

It was a classic speculation bubble.

Then in late 2006–2007, that bubble burst.

The housing market became oversupplied. People stopped buying the new construction and the existing homes as much. And home values started to drop.

And suddenly, because home values plateaued and then dropped, so too did the little bit of equity that many of these purchasers, in debt up to their eyeballs, had in their homes. Without more equity, they couldn’t refinance. And because they could’t refinance, those ARM loans or other loans kicked in, and the interest rates on them skyrocketed.

And suddenly, they couldn’t make the payments anymore.

And then they went into default on their mortgages.

Followed by foreclosure.

And often bankruptcy.

It turned into a vicious cycle. Once one or two neighbors end up losing their homes in foreclosure, it affects the property values of everyone else around those properties like a contagion. Healthier borrowers started to become impacted as property values declined and now they couldn’t refinance.

In 2007, lenders foreclosed on 79% more homes than in 2006: 1.3 million foreclosures. In 2008, this skyrocketed another 81% still: 2.3 million. By August of 2008, nearly one in ten mortgages nationally were in default and foreclosure proceedings. By one year later, this had risen to over 14% nationally.

The Recession

Remember, the financial sector had heavily invested in all of those housing market securities. They thought they were safe. They thought that the housing market would never go anywhere but up. They built their whole foundation on it.

And they had relied on those securities to meet their capitalization requirements.

Securities that suddenly turned out to be nearly worthless.

Huge banks ran out of liquid cash almost immediately. This is what happened to Bear Stearns, Lehman Brothers, Goldman Sachs, Citibank, and more. They were suddenly holding on to billions upon billions of dollars of assets that were either worthless, or completely frozen. They couldn’t sell the bits of stuff that was even worth anything.

And because their assets weren’t liquid, they didn’t have money to lend anymore.

And that lack of credit is what grinds the economy to a halt.

That impacted every sector of business in the United States. Which impacted every sector of business in the world. And that meant that businesses started having to lay people off because they couldn’t get the money to keep paying them.

And then because those people lost their jobs, they started to default on their mortgages. Which rippled through the CDO market again.

This was why it was so critical for the Federal Reserve to buy those toxic assets and provide the banks with liquid cash in their place. They had to get the credit flowing again to re-start the gears of the economy. Without it, we almost certainly would have seen a full repeat of the Great Depression.

And that brings us to today.

That’s the abbreviated, oversimplified explanation. It’s more complicated than this, and there’s other factors that contributed, but that’s kind of the main story in basic terms. That’s roughly how 10 million homes went into foreclosure.

And we still haven’t fully recovered. Over twice as many people rent as opposed to own. Less than one-third of people who have lost a home in foreclosure in the last decade will be able to repurchase another again. Roughly 2/3ds of those people who lost their homes have so damaged their credit that they will never qualify again. Hundreds of thousands, if not millions more, were so emotionally traumatized by the experience that they simply refuse to go through it again.

And that number of renters to owners is substantially higher for my generation, the Millenials, who have never seen any substantial portion of the post-2008 recovery. We still haven’t made up the wages that would allow us to save enough to purchase, even setting aside the massive increase in student debt we carry.

75% of my generation wants to own a home. Less than 35% do.

And, in case reading this wasn’t chilling enough for you, the present administration has been lifting some of the exact rules and regulations that were put into place after the 2008 collapse that were lifted in 2004 that were put in place after the 1980’s collapse after those were lifted. Because it worked so well the first two times.

Mostly Standard Addendum and Disclaimer: read this before you comment.

I welcome rational, reasoned debate on the merits with reliable, credible sources.

But coming on here and calling me names, pissing and moaning about how biased I am, et cetera and BNBR violation and so forth, will result in a swift one-way frogmarch out the airlock. Doing the same to others will result in the same treatment.

Essentially, act like an adult and don’t be a dick about it.

- Look, this is pretty oversimplified. Ph.D. theses have been written about this. I’m trying to make it at least remotely accessible to those with the patience to read it. Don’t be pedantic about it, please?

- Getting cute with me about my commenting rules and how my answer doesn’t follow my rules and blah, blah, whine, blah is getting old. Stay on topic or you’ll get to watch the debate from the outside.

- Same with whining about these rules and something something free speech and censorship.

- If you want to argue and you’re not sure how to not be a dick about it, just post a picture of a cute baby animal instead, all right? Your displeasure and disagreement will be duly noted. Pinkie swear.

If you have to consider whether or not you’re over the line, the answer is most likely yes.

Debate responsibly.

You can also access the latest news at this address: www.whatfinger.com

-

WARNING!!! The prophet Isaiah warns us that in the last days God is going to “turn the world upside down.”

This article has been updated and republished again, because it had a massive impact on the general public and I think it deserves to be shared with you again!

The prophet Isaiah warns us that in the last days God is going to “turn the world upside down.” He declares, “Behold, the Lord maketh the earth empty, and maketh it waste, and turneth it upside down” (Isaiah 24:1).

According to this prophecy, sudden judgment is coming upon the earth, and it will change everything in a single hour. Within that short span, the whole world will witness fast-falling destruction upon a city and a nation, and the world will never be the same.

If you are attached to material things — if you love this world and the things of it — you won’t want to hear what Isaiah has prophesied. In fact, even to the most righteous of God’s people, what Isaiah says might seem unthinkable. Many would surely ask, “How can an entire world be stricken in one hour?”

If we didn’t believe the Bible is God’s pure Word, few of us would take Isaiah’s prophecy seriously. But Scripture makes it clear: in a single hour, the world is going to change. The church is going to change. And every individual on earth is going to change.

The apostle John gives a similar warning in Revelation. He speaks of destructive judgment coming upon a city and nation: “In one day, death, and mourning, and famine; and she shall be utterly burned with fire: for strong is the Lord God who judgeth her…. For in one hour so great riches is come to nought” (Revelation 18:8, 17).

In Isaiah’s prophecy, the city under judgment is cast into confusion. Every house is shut up, with no one coming or going. “The city of confusion is broken down: every house is shut up, that no man may come in” (Isaiah 24:10). The entire city is left desolate: “In the city is left desolation, and the gate is smitten with destruction” (24:12). All entrances and exits to the city are gone. The passage indicates that a fire has come, a blast that has shaken the very foundations of the earth (see 24:6).

We who live in New York City know something about this kind of scene. When the Twin Towers were attacked, the ominous fires and smoke could be seen ascending to heaven for miles. Recently, New Yorkers panicked as a mass of steam erupted from below a city street. People ran in all directions screaming, “Is this it? Is this the end-all attack?”

Today, multitudes of secular prophets are saying a nuclear attack is inevitable. The target they mention most often is New York, but it could happen in any major city: London, Paris, Tel Aviv, Washington. Neither Isaiah nor John names the city upon which destructive judgment falls.I don’t intend this message to frighten anyone.

Let me make clear at this point: I don’t intend this message to frighten anyone. Paul tells us that as disciples of Jesus Christ, we have already passed from death into life. We who call on Jesus as Lord should be confident that no matter what happens in this world, his shed blood saves and redeems us.

Therefore, we are not to fear any newscast, but rather to be attentive to what the Lord is doing in the world. Like many people, I hear grievous reports that make me want to tune everything out. But the truth is, God moves in the midst of such times, and through them he speaks warnings to all who would hear his voice.Isaiah’s prophecy points clearly to our generation.

I believe, along with many eminent Bible scholars, that Isaiah’s prophecy points to the last days. By that, I mean our present time. In short, sudden judgment is coming, and Scripture strongly indicates it is now at the door.

At this point you may be wondering: “How can we be sure we’re the generation this prophecy points to?” We can know by two reasons that such judgments are imminent:

1.A growing number of prophets warn of an apocalyptic disaster at the door. When I use the word “prophets,” I speak not just of those in the church. I’m talking also about “secular prophets.”

There are several precedents for secular prophets in Scripture. God used Assyria as his rod of correction with Israel. And he appointed King Cyrus as his servant to assist Israel: “(The Lord) saith of Cyrus, He is my shepherd, and shall perform all my pleasure” (Isaiah 44:28).

Likewise today, God uses secular prophets to send warnings. These become “his prophets” for a season. And their prophecies can be harder than those delivered by believers. The message I’m writing here is mild compared to the prophecies being delivered by all manner of secular voices. Just check your newspaper or radio reports.

“Surely the Lord God will do nothing, but he revealeth his secret unto his servants the prophets” (Amos 3:7).

2.Sudden destruction comes when the cup of violence overflows. Sensuality, perversion and greed are running rampant throughout our society. Yet, when God sent the Flood upon the earth, it was because of a worldwide eruption of violence: “The earth also was corrupt before God, and the earth was filled with violence” (Genesis 6:11).

Right now, there are numerous wars and bloody uprisings taking place around the globe. Yet foremost in my mind is the violence being waged against children worldwide:

- I think of the sexual violence of pedophiles. Children all over the world are being raped, kidnapped and forced into enslavement in the global sex trade. Recently, a pedophile in the U.S. was discovered running a web site that advises other pedophiles on the easiest places to pick up children. There is no law in place to stop this man. The world’s largest church denomination has spent hundreds of millions of dollars to settle the claims of those who were molested in childhood by clergy. Tell me, how long will God endure the pitiful cries of children who are molested by those who would represent Christ?

- Thousands of children in Africa are being slaughtered in tribal wars, hacked to death by machetes. Young boys — even those under ten years of age — are enlisted into tribal militias and forced to murder men in initiation rites.

- Here in the U.S., the blood of millions of aborted babies cries out from the ground.

- Reports of school murders no longer shock many of us but continue to terrorize our children. We may grow hardened to such reports, but God’s heart is grieved by them.

I tell you, there is no worse violence than the brutalizing of children. Heaven is crying out, “Woe, woe! Your judgments have no cure.”1. In one hour, God is going to change the whole world.

A sudden cataclysmic event will strike, the first of the final judgments of God. This great event will cause the earth to reel. And Isaiah says that when it hits, there will be no place to escape: “The lofty [proud] city, he layeth it low…even to the ground; he bringeth it even to the dust” (Isaiah 26:5). “The inhabitants of the earth are burned” (24:6).

Once this happens, utter chaos will erupt. All civic activities will stop, and society will descend into massive disorder. Government agencies will be helpless to restore any kind of sanity. No state troopers, no national guard, no army will be able to bring order to the upheaval.

You well remember that when the Twin Towers were destroyed, help poured into New York from all over the world. An army of people came to assist in whatever way they could. But the scene in Isaiah’s prophecy is different: this calamity is clearly beyond humankind’s capacity to respond.

Once this judgment strikes, it will devastate the economy. Rich merchants will stand by watching in torment, weeping and mourning, as they face bankruptcy. In an instant, all the wealth they amassed will be reduced to nothing. John describes the scene: “The merchants of these things, which were made rich by her, shall stand afar off for the fear of her torment, weeping and wailing, saying, Alas, alas that great city… For in one hour so great riches is come to nought” (Revelation 18:15–17).

Overnight, all buying and selling will cease. Every restaurant and bar will be shut down, and all drinking and music making will end. Indeed, every trace of mirth and delight, joy and gladness, will vanish: “All the merryhearted do sigh. The mirth of tabrets ceaseth, the noise of them that rejoice endeth, the joy of the harp ceaseth. They shall not drink wine with a song…. The mirth of the land is gone” (Isaiah 24:7–9, 11).

Yes, this is a picture of gloom and doom. But it is not my prophecy. This word was given by the Holy Spirit of Almighty God, to be delivered by his righteous prophet Isaiah. Even the secular world is preparing for it to happen. Billions are being spent on homeland security in the U.S., England, Europe and Israel. Why? Military experts warn that a world-impacting terrorist attack is sure to come.

You may ask: “Why would the whole world change, if a nuclear attack occurs in just one city?” It will happen because of the fear of retaliation. If a rogue nation sends such an attack, you can be sure that within hours that nation will be wiped out. Consider the plan Israel has in place, known as the Samson Option. The moment a nuclear warhead is launched against them, within moments Israel will unleash nuclear missiles to devastate the capital cities of all enemy states.

The world has become a ticking bomb, and time is quickly running out.2. In one hour, God is going to change the church.

This hour of devastation will suddenly change churches, whether they are alive or dead. Isaiah writes, “There shall be the shaking as of an olive tree” (Isaiah 24:13). The image is of God shaking an olive tree after it has been picked of fruit. In short, he’s going to shake everything that can be shaken, sparing nothing. It will be a time of cataclysmic destruction and overwhelming darkness.

So, you ask, “What about God’s people in the midst of all this? What will happen to the church?” Isaiah gives us an incredible word about what will happen with believers.

In the midst of the terrible shaking, a song will be heard, and its sound will grow steadily stronger. Suddenly, in that darkest of hours, a worldwide chorus of voices will sing praises to the majesty of God: “They shall lift up their voice, they shall sing for the majesty of the Lord, they shall cry aloud from the sea” (24:14).

Do you get the picture? There will be panic everywhere. Men’s hearts will fail them for fear, as fires belch smoke seen for hundreds of miles. Disorder and chaos will reign on all sides. Yet amid the devastating fires and calamity, the world will hear a glorious song being sung: “Glorify ye the Lord in the fires, even the name of the Lord God of Israel… From the uttermost part of the earth have we heard songs, even glory to the righteous [One]” (Isaiah 24:15–16).

A holy remnant is going to awaken, and a song will be born in the fire. Instead of panicking, the people of God will be praising his awesome majesty. Imagine it: in the darkest hour of all time, a collective voice will rise by the millions out of every nation, not in fear or agony, but in joyful praise to the Lord.

How will this happen, you ask? In one hour, God is going to regenerate and restore his church. Dry bones will shake and rattle, and the righteous will be awakened, as the Holy Spirit calls multitudes of lukewarm believers back to their first love. In his mercy, he’s going to rouse those who have neglected him, ignoring his Word, avoiding prayer, perhaps even contemplating divorce. Suddenly, their souls will be flooded with pangs of remorse and godly sorrow. And many will fall on their knees, crying out in repentance.

There will be a revival of glorifying God’s majesty. And the song of this revival will be heard from the uttermost parts of the earth. East, west, north and south — from Arab lands to China, Indonesia, Africa and all parts of the earth — a glorious song will rise up from the midst of the fires. In one day’s time, those who survived the fires are going to be singing a new song throughout the world.Isaiah 25 tells us wonderful miracles will come in this time, as “God makes all things new.”

All around the world, the Lord’s people are going to “feast” on his Word: “In this mountain shall the Lord of hosts make unto all people a feast of fat things, a feast of wines on the lees, of fat things full of marrow, of wines on the lees well refined” (Isaiah 25:6).

“And he will destroy in this mountain the face of the covering cast over all people, and the veil that is spread over all nations” (25:7). Right now, in this time of prosperity, the world’s masses seem to be covered with a veil, unable to see the truth of Jesus Christ. But when God rises up to shake the world through judgment, the shrouds covering the minds of billions will be cast aside. The veil of darkness will be removed, and many will see the Lord in his glory. The Holy Spirit won’t force Christ upon these opened eyes and hearts; rather, a remnant is going to rise up from among them.

I believe the darkest shroud-coverings today are over the eyes and hearts of youth worldwide. This is especially true of college-age students, whose faith has been bombarded for up to four years. Over that time their minds have been indoctrinated by godless professors in classrooms where belief is attacked, mocked and scorned. Now these young men’s and women’s faith has been shipwrecked. They leave college convinced God is dead.

But in one hour of devastation — nuclear, economic and social — all such hypocritical veils are going to fall away. Those same professors who mocked them will realize, as they face the possibility of death, a choice must be made: “What about eternity? Is there life after death?” They’re going to look for someone to explain to them all that’s happening.

When the song is sung, it’s going to be heard by young people from every walk of life, from every nation under the sun. Many will harden their hearts and curse God at the sound of this song, but multitudes of others will join in singing of his majesty.3. In one hour, God is going to change us as individuals.

In a single hour, the focus of our lives will be changed. We’ll no longer obsess about our own adversities and troubles. Suddenly, so many things that we held dear will no longer be of any value to us. Why? In that hour, everyone will be in the same boat:

“It shall be, as with the people, so with the priest; as with the servant, so with his master; as with the maid, so with her mistress; as with the buyer, so with the seller; as with the lender, so with the borrower; as with the taker of usury, so with the giver of usury to him” (Isaiah 24:2).

The sudden judgment that comes will not be a respecter of anyone. Rather, it is going to touch all who are within the realm of its fury. Presidents, kings, the world’s richest and most famous — all will tremble just like the poorest of the earth. And this cataclysmic event will bring to naught every idol, purging iniquity and tearing down all false altars:

“By this [the calamity] therefore shall the iniquity of Jacob be purged; and this is all the fruit to take away his sin; when he maketh all the stones of the altar as chalkstones that are beaten in sunder, the groves and images shall not stand up [be left standing]” (Isaiah 27:9).

The world’s most prominent idol is money, and right now America is facing a monstrous financial disaster. Investors are scrambling to move their money out of high-risk funds, and mortgage companies are going bankrupt. One recent financial headline read, “Abandon Ship!” Everyone is selling and nobody is buying. Many households are in a panic, as overnight their lives are changing. I think of the president of a multi-billion-dollar hedge fund, who recently put up for sale his 142-foot yacht and his sixteen-bedroom mansion in Aspen, Colorado. His fund had dried up virtually overnight.

The day is coming when sports will be the last thing on people’s minds. I have nothing against sports, but soon there will be no more 250-million-dollar deals for athletes, when so much of the world is starving. All idols will come crashing down, crushed to dust, and the playing field will be leveled. The richest and the poorest alike will face the same conditions.

It will all happen within a day. “When they shall say, Peace and safety; then sudden destruction cometh upon them, as travail upon a woman with child; and they shall not escape” (1 Thessalonians 5:3).Why such apocalyptic warnings?

You may wonder: what good can come of these prophetic messages? Why should anyone have to live under such anxiety?

I remind you, Jesus warned Jerusalem of sudden devastation to come upon that city. It was going to be burned to the ground, with over a million people murdered. Christ explained his warning: “I have told you before it come to pass, that, when it is come to pass, ye might believe” (John 14:29). He was saying, in essence, “When it happens, you’ll know there is a God who loves you and forewarned you.”

Paul calls such warnings “light,” insights that expel darkness. He says, in short: “You are children of light, because you know what’s coming in the future. So, when destruction comes, and there’s panic all around, you will have the calm of the Holy Spirit. Something will quicken inside you, and you’ll remember, ‘God warned me.’ This prophecy isn’t a message of wrath to God’s people, but a wakeup call to begin preparing.”

“God hath not appointed us to wrath, but to obtain salvation by our Lord Jesus Christ, who died for us, that, whether we wake or sleep, we should live together with him” (1 Thessalonians 5:9–10). Paul is speaking here of a time of possible destruction. Therefore, he says, “Comfort yourselves together, and edify one another, even as also ye do” (5:11).

In this day of prosperity, nobody wants to hear a message like Isaiah’s. I certainly don’t want to hear it. But we cannot ignore it, because it is here at our door. In such times, Paul says, when we have knowledge that sudden destruction is coming, we are not to tremble or sorrow as the world does. Instead, we are to comfort one another in faith, knowing that God rules over every aspect of our lives.

“Be sober, putting on the breastplate of faith and love; and for an helmet, the hope of salvation” (5:8). Paul instructs, “Arm yourself with faith. Build up your belief now, before the day comes. Learn your song, and you’ll be able to sing it in your fire.” “Glorify ye the Lord in the fires, even the name of the Lord God of Israel” (Isaiah 24:15).

This is the hope of our most holy faith: our Lord causes a song to come out of the darkest of times. Start now to build up your holy faith in him, and learn to praise his majesty quietly in your heart. When you sing your song, it will strengthen and encourage your brothers and sisters. And it will testify to the world: “Our Lord reigns over the Flood!” ■

You can also access the latest news at this address: www.whatfinger.com

-

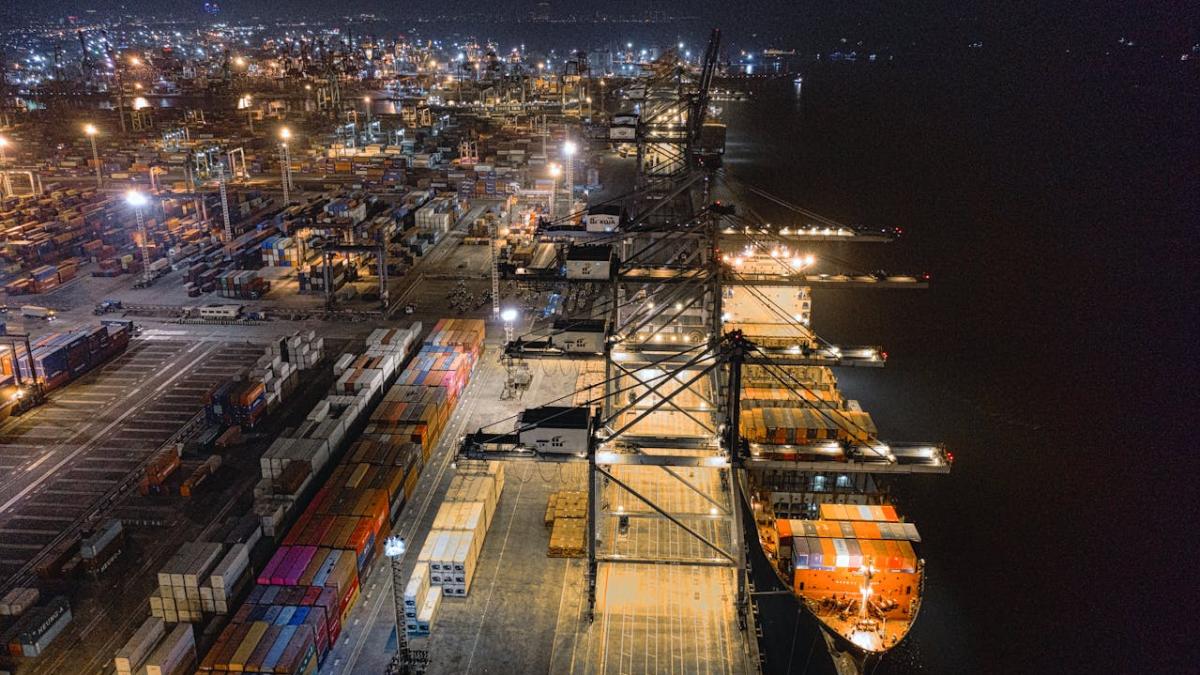

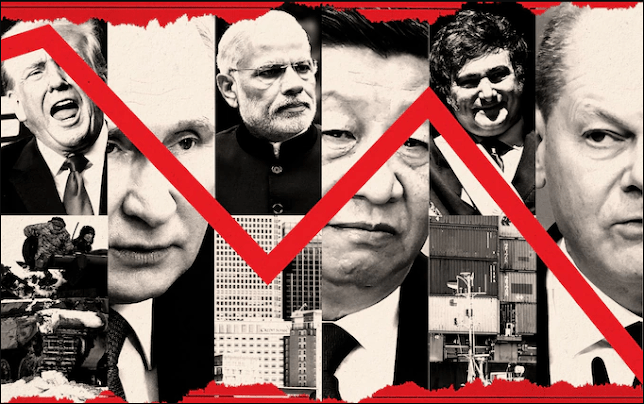

How The Trade War Ends (These wars start as currency and trade wars and then escalate into shooting wars. Only the complete devastation and destruction of a world war, and a full reset to the power balance, will bring a trade war to its bitter end)

The quote “When goods don’t cross borders, soldiers will,” is frequently attributed to 19th century writer and free market economist Frederic Bastiat. While these specific words, strung together with this specific syntax, cannot be found in Bastiat published catalogue, their sentiments are of the type he would have likely endorsed.

The point is that free trade not only increases the wealth of different societies, but it may also be essential for peaceful relations. The breakdown of free trade has often coincided with wars. These wars start as currency and trade wars and then escalate into shooting wars. This is something to be mindful of as President-elect Trump amps up forthcoming import tariffs.

Global trade has expanded without interruption for so long that only senior citizens remember anything different. But global trade hasn’t always expanded. In fact, there have been long episodes of global trade contractions that have played out over long secular trends for thousands of years.

The Silk Road, for example, was established by the Han Dynasty of China in 130 BC. This ancient route allowed for continuous trade between east and west for nearly 1,600 years. The Silk Road was not only a conduit for the exchange of goods. It was also a conduit for the exchange of culture and knowledge – and plagues and diseases – among its network of civilizations.

Like other features of civilization that once appeared to be permanent, this trade route eventually came to an end. When the Byzantine Empire fell to the Turks in 1453 AD, the Ottoman Empire closed the Silk Road and cut all ties with the west. Geopolitical trends between the east and west turned inward towards isolation.

Declining Global Trade

Global trade these days is conducted by shipping cargo across the international waters of the high seas. Trade cycles over the last 200 years have often expanded for such lengthy durations that several generations will come and go while only knowing the expansionary half of the trend. These extended expansionary episodes compel people to believe that increased global trade is a linear phenomenon.

You have to go back to pre-1960 in the United States, Japan, and Western Europe to find someone with living memory of a global trade contraction. China’s latest trade expansion began in the 1970s. Eastern Europe’s began in the early 1990s.

Those willing to look back to the first half of the 20th century will discover something that goes counter to their life experience. Global trade, as a proportion of total economic activity, went down between the onset of World War I and the 1960s. That’s a nearly 50-year run of declining global trade.

We posit that the breakup of the classical gold standard at the onset of the Great War had something to do with this. Eastern Europe suffered rampant hyperinflation in the 1920s while in the USA the inflation manifested in an epic stock market bubble.

When that went kaput, and the world spiraled into the Great Depression, the Smoot-Hawley Tariff Act of 1930, and tit for tat retaliatory tariffs, took an axe to what remained of global trade. It also presaged the start of World War II.

It wasn’t until well after WWII that international trade picked back up. This trade, while hesitant at first, blossomed during the latter part of the 20th century. Nonetheless, that doesn’t mean trade will continue to expand indefinitely.

Political Intervention

Geopolitical shocks have periodically disrupted or reversed overall long-term trends in expanding global trade. The World Trade Organization publishes a World Trade Report each year documenting the state of international trade and offering various facts and anecdotes. If you peruse through them, you can find interesting insights. For example, the World Trade Report 2013 included this nugget:

“Politics [at times] has intervened – sometimes consciously, sometimes accidentally – to slow down or even roll back the integrationist pressures of technology and markets. It is this complex interplay of structural and political forces that explains the successive waves of economic integration and disintegration over the past 200 years; and in particular how the seemingly inexorable rise of the ‘first age of globalization’ in the 19th century was abruptly cut short between 1914 and 1945 – by the related catastrophes of the First World War, the Great Depression and the Second World War – only to be followed by the rise of a ‘second age of globalization’ during the latter half of the 20th century.”

There are times when extrapolating from the economic past and projecting into the future are exceedingly thoughtless and blind. Right now, maybe one of those times. By our estimation, the potential for multiple geopolitical shocks, including wars and currency chaos, to interrupt or reverse the global trade expansion that has been in place since the 1960s is extremely high.

At the moment, it’s very well possible that we’re near the start of another long-term global trade contraction. The impetus of the trade contraction is a politically motivated trade war.

Trump campaigned on a promise to impose at least a 60 percent tariff on Chinese imports. The intended purpose is to correct the ghastly $300 billion annual trade deficit the U.S. has with China and to remake the USA into a manufacturing powerhouse.

Somehow, trade tariffs will make it possible for factory jobs to return to America’s rustbelt so the country can experience the nirvana of full MAGA. Moreover, in doing so, the forgotten workers of America will be able to kick their fentanyl addiction.

This all sounds great. But will a full-on trade war attain the desired result for the USA. We may soon find out in real time…

How The Trade War Ends

A trade war, in simplest terms, will result in a trade contraction. Shrinking trade means less imported and exported goods. Less imported and exported goods means smaller economic growth. Smaller economic growth means less wealth creation.

In short, a trade war means a smaller economy. It also means a reduction in choices, and a shrinking of global wealth.

For American consumers, with their heavy dependence on imported goods, it means higher prices. It also means fewer choices.

As the trade war escalates, all sorts of strange and dysfunctional things will happen. American visitors to China may discover high quality Electric Vehicles, made by companies they’ve never heard of, selling for just $10,000 a pop.

These brands and bargain prices will be effectively excluded from American markets. At the same time, American workers will earn $20 per hour to make socks, which will quadruple their price.

Regardless, Trump is committed to sticking it to other countries with across-the-board tariffs of 10 to 20 percent as part of his America First economic policy. For China, he’s reserved a special 60 percent tariff.

The purpose of these tariffs, in addition to potentially increasing Made in the USA goods, is to generate revenue to offset Trump’s tax cuts. Import tariffs in combination with domestic tax cuts would drive import volumes down while household and business spending would increase. This is a recipe for rising consumer price inflation.

There’s also the potential of this politically motivated trade war leading to a world war. What then? Can the consequences be undone before it’s too late?

Alas, the historical precedent is less than cheerful.

Once a global trade war starts in earnest there really isn’t a quick end. Like a California wildfire, once the conflagration starts it cannot be stopped.

Only the complete devastation and destruction of a world war, and a full reset to the power balance, will bring a trade war to its bitter end.

You can also access the latest news at this address: www.whatfinger.com

-

Gun Control Master Plan- What To Do When Gun Control Gets Really Bad

MUST WATCH THIS VIDEO: Free Power Secrets! Revealed: The century-old device making solar panels obsolete. Embrace efficient, sustainable energy. Open the Gates of Innovation!

Gun Control is a favorite tactic for many politicians on the left. It allows them to shift the blame from the person, whose worldviews and political party often aligns with theirs, to a simple tool they can ban. With an all Republican everything, you’d think we wouldn’t have to worry, but that’s far from true. These people seemingly always find a way to infiltrate politics and attempt to strip us of our God-given rights. So what do we do? How do we fight back if gun control legislation is proposed or passed?

#1. Learn How To Make Your Own

California is the beacon of cruddy gun control laws in the United States. They’ve gone above and beyond to reclassify your standard semi-automatic rifle into what they call an assault rifle. What we’ve seen is people and companies outsmarting the legislature at every turn. One of the most famous means was building your own gun. Specifically AR 15s. AR 15s are always on the chopping block, but even California couldn’t stop the signal.

With the advent of 80% lowers Californians were able to again build their own rifles within the law. The AR 15 is hardly the only weapon you can build. In fact, an enterprising patriot build can manufacture their own semi-auto Sten gun, Glocks, MAC 10/11s, AK rifles and more. The main issue is going to be acquiring the skills and tools needed to make these weapons. It takes a little mechanical skill and a lot of different tools.

It would be wise to start learning the insides and outsides of guns now. Learn to build them, acquire the tools, and fire up the Youtube machine. Here you’ll find as hard as they try they can’t stop the signal. You can build your own with a little practice, and it’s perfectly legal to do so. You aren’t just building guns, you are learning valuable skills regarding the construction and design of firearms that could be invaluable if things got really bad.

The summer 2024 training was explicit: the government practiced suppressing dissent. This included the simulated arrest of American citizens who opposed federal policies. FEMA is now implementing the logistical groundwork laid during that exercise.

#2. Recognize the Gun Ban Matrix

One fact we’ve seen over and over again with anti-gunners is that they know absolutely nothing about guns. If the power these people had wasn’t so terrifying it would be hilarious. Every time they open their mouths about guns they say something incredibly stupid. They simply target guns that look scary and that’s it. That’s why the gun ban matrix exists. The gun ban matrix is a list of features and guns unlikely to be banned because anti-gunners are idiots and don’t understand firearms.

These are the guns you should consider investing in should sweeping legislation occur. In case the situations getting drastic and confiscation begins things may move too fast for people to react. In that event a neutered gun is better than no gun.

The first guns to go are going to be the traditional targets for anti-gunners, the AK 47s, the AR 15s, the Tavors, and the usual suspects. They may be banned by name, or by the features they share. A good alternative to these semi-auto rifles is the Ruger Mini 14 and Mini 30 series. They can be purchased in not so scary configurations.

Past the Mini 14 and Mini 30, there is the fixed magazine SKS rifle. It’s often left off ban lists, and it’s affordable and common. It’s limited to ten rounds, but with stripper clips, you can reload quite fast with practice.

Past this level we get into manually operated firearms, this includes pump-action shotguns, and lever and bolt action rifles. A good lever action rifle is a rapid firing gun and in the right caliber can hold up to 14 rounds. These guns are highly unlikely to be banned without a full constitutional amendment.

#3. Don’t Give A Single Inch

With the recent Las Vegas shooting there has been an increased interest in banning a firearm accessory known as a bump fire stock. These accessories are rather dumb and useless, and in no way did it make the shooter more lethal. Regardless of how dumb and useless they are there is no reason the firearms community should let them be banned without a fight. With the NRA even saying the ATF should reevaluate bump fire stocks.

This is how gun control starts, with tiny little cuts. We let them take one dumb accessory and next time they’ll push for something else, and they’ll keep pushing. Give them nothing, not a single inch. As gun rights advocates we have to defend what we have and go on the offensive. Fight back and take our God Given rights back.

#4. Push Back and Push Back Hard

If legislation gets passed regarding gun control, and I mean any legislation at all, we have to push back. The vast majority of gun owners are law abiding, tax paying, job having citizens who want nothing more than to live in peace. We all know actual gun control will do absolutely nothing to strip criminals of firearms, just good people who already obey the law.

If gun control happens as law abiding gun owners we have to flood the legislator’s offices with our demands. We have to protest, we have to write letters, we need to march on the capitals. In 2012 the gun community did an amazing job of coming together to resist any form of gun control. We need that same response to every law that passes, heck we need that reaction every gun control law that is even proposed.

We need to push at the local, state and federal level. Work every angle possible. We have to keep supporting companies that agree with our God-given rights, we have to join gun rights organizations of every kind. We literally have to put our money where our mouth is.

#5. Focus on the Small Politics as Much as the Large

It’s easy to forget the importance of local politics when it comes to federal gun control. Local and state politics can make all the difference. We saw Sheriff’s in states across the union step forward and say they would refuse to enforce federal gun control laws in their counties. We saw states and municipalities adopt laws that would act to nullify federal gun control laws.

If we can’t toss the anti-freedom and anti-gun bastards out of federal offices we can at least elect the right people at the local and state level to ensure the laws are useless.

Resist

As American citizens, we owe it to future generations to resist. Resist with every fiber we have. Resist gun control measures with everything we can. We need to prepare for the worst and always ready to resist.

This guide below can help you in a survival situation

A lot of the popularity of firearms is due to the fact that anyone can use them effectively, not only the strong and agile. The young, the old, men, women and child can take up firearms in defense of home and family and do so effectively.

But what do you do if you can’t use a gun – or if you don’t have a gun — to protect yourself?

-

20 Things You Will Need to Survive When the Economy Collapses and the Next Great Depression Begins

Today, millions of Americans say that they believe that the United States is on the verge of a major economic collapse and will soon be entering another Great Depression. But only a small percentage of those same people are prepared for that to happen. The sad truth is that the vast majority of Americans would last little more than a month on what they have stored up in their homes. Most of us are so used to running out to the supermarket or to Wal-Mart for whatever we need that we never even stop to consider what would happen if suddenly we were not able to do that. Already the U.S. economy is starting to stumble about like a drunken frat boy. All it would take for the entire U.S. to resemble New Orleans after Hurricane Katrina would be for a major war, a terror attack, a deadly pandemic or a massive natural disaster to strike at just the right time and push the teetering U.S. economy over the edge. So just how would you survive if you suddenly could not rely on the huge international corporate giants to feed, clothe and supply you and your family? Do you have a plan?

Unless you already live in a cave or you are a complete and total mindless follower of the establishment media, you should be able to see very clearly that our society is more vulnerable now than it ever has been. This year there have been an unprecedented number of large earthquakes around the world and volcanoes all over the globe are awakening. You can just take a look at what has happened in Haiti and in Iceland to see how devastating a natural disaster can be. Not only that, but we have a world that is full of lunatics in positions of power, and if one of them decides to set off a nuclear, chemical or biological weapon in a major city it could paralyze an entire region. War could erupt in the Middle East at literally any moment, and if it does the price of oil will double or triple (at least) and there is the possibility that much of the entire world could be drawn into the conflict. Scientists tell us that a massive high-altitude EMP (electromagnetic pulse) blast could send large portions of the United States back to the stone age in an instant. In addition, there is the constant threat that the outbreak of a major viral pandemic (such as what happened with the 1918 Spanish Flu) could kill tens of millions of people around the globe and paralyze the economies of the world.

But even without all of that, the truth is that the U.S. economy is going to collapse. So just think of what will happen if one (or more) of those things does happen on top of all the economic problems that we are having.

Are you prepared?

The following is a list of 20 things you and your family will need to survive when the economy totally collapses and the next Great Depression begins….

#1) Storable Foo

Food is going to instantly become one of the most valuable commodities in existence in the event of an economic collapse. If you do not have food you are not going to survive. Most American families could not last much longer than a month on what they have in their house right now. So what about you? If disaster struck right now, how long could you survive on what you have? The truth is that we all need to start storing up food. If you and your family run out of food, you will suddenly find yourselves competing with the hordes of hungry people who are looting the stores and roaming the streets looking for something to eat.

Of course you can grow your own food, but that is going to take time. So you need to have enough food stored up until the food that you plant has time to grow. But if you have not stored up any seeds you might as well forget it. When the economy totally collapses, the remaining seeds will disappear very quickly. So if you think that you are going to need seeds, now is the time to get them.

#2) Clean Water

Most people can survive for a number of weeks without food, but without water you will die in just a few days. So where would you get water if the water suddenly stopped flowing out of your taps? Do you have a plan? Is there an abundant supply of clean water near your home? Would you be able to boil water if you need to?

Besides storing water and figuring out how you are going to gather water if society breaks down, another thing to consider is water purification tablets. The water you are able to gather during a time of crisis may not be suitable for drinking. So you may find that water purification tablets come in very, very handy.

#3) Shelter

You can’t sleep on the streets, can you? Well, some people will be able to get by living on the streets, but the vast majority of us will need some form of shelter to survive for long. So what would you do if you and your family lost your home or suddenly were forced from your home? Where would you go?

The best thing to do is to come up with several plans. Do you have relatives that you can bunk with in case of emergency? Do you own a tent and sleeping bags if you had to rough it? If one day everything hits the fan and you and your family have to “bug out” somewhere, where would that be? You need to have a plan.

#4) Warm Clothing

If you plan to survive for long in a nightmare economic situation, you are probably going to need some warm, functional clothing. If you live in a cold climate, this is going to mean storing up plenty of blankets and cold weather clothes. If you live in an area where it rains a lot, you will need to be sure to store up some rain gear. If you think you may have to survive outdoors in an emergency situation, make sure that you and your family have something warm to put on your heads. Someday after the economy has collapsed and people are scrambling to survive, a lot of folks are going to end up freezing to death. In fact, in the coldest areas it is actually possible to freeze to death in your own home. Don’t let that happen to you.

#5) An Axe

Staying along the theme of staying warm, you may want to consider investing in a good axe. In the event of a major emergency, gathering firewood will be a priority. Without a good tool to cut the wood with that will be much more difficult.

#6) Lighters Or Matches